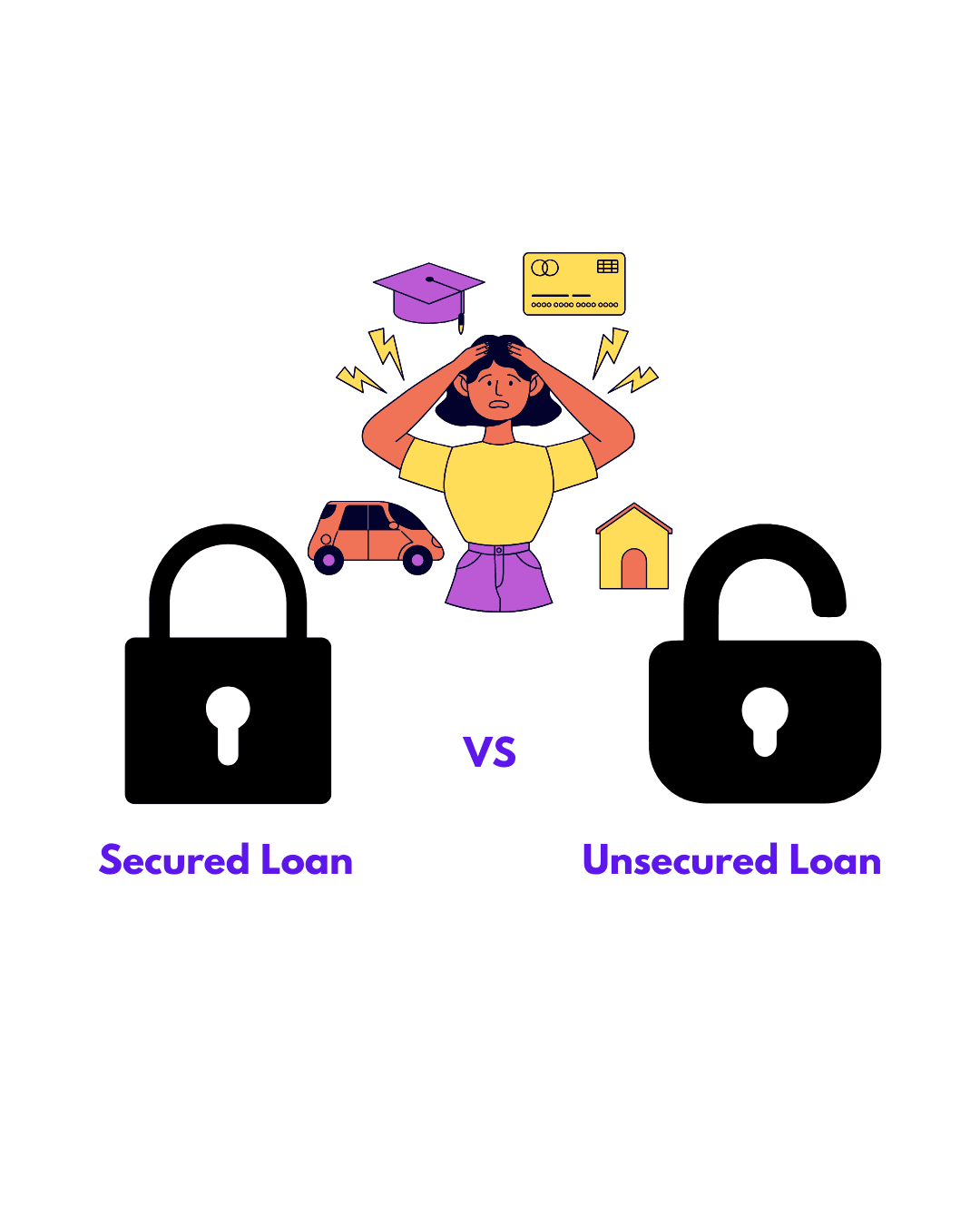

Difference Between Secured and Unsecured Loans: What You Need to Know

Introduction: Why Does This Loan Difference Truly Matter?

When considering taking a loan—to buy a house, to pay for a wedding, or to cover an unexpected expense—being aware of the type of loan you are seeking is important. In India, lenders classify loans into two main types: secured and unsecured loans.

Every type of loan has its own set of rules, risks, and advantages. The contrast can affect everything from your rate of interest to how much money you are allowed to borrow and how stern the terms of repayment are. Whether you’re shopping for a new car or simply need some quick cash in hand, you will be better prepared to make wise financial choices if you are aware of every aspect of these loans.

What is a secured loan?

Definition & How it Works

A secured loan is distributed according to collateral. What it means is that when you are taking a loan, you’re using an asset—your car, property, or fixed deposit—to serve as a guarantee. In case of non-repayment of the loan, the lender has the right to seize and auction the asset to reclaim the amount.

These are less risky loans to lenders, they are usually charged at a low interest rate, a long tenure, and a larger loan amount.

Examples of Secured Loans in India

- Home Loan: You use your property as collateral. The lender takes possession if you fail to repay.

- Car Loan: Your car itself will serve as the collateral.

- Loan Against Property (LAP): Use your commercial or residential property to borrow money by pledging it as security.

- Loan Against Fixed Deposit or Gold: Your gold and/or fixed deposits are used as collateral.

Key terms to remember:

- Collateral: The property you promise to the lender.

- Loan-to-Value (LTV) Ratio: The highest percentage of the asset’s value you are allowed to borrow.

- Foreclosure: The lender takes possession of your asset if you are unable to pay it back.

What is an unsecured loan?

Definition & How it Works

Unsecured loans do not involve any collateral. The loans are advanced on the basis of credit score, income, job stability, and loan eligibility. As the risk is higher on the part of lenders, the rate of interest is higher and the term is shorter.

These loans are best suited to individuals who require instant cash and don’t wish to mortgage their belongings.

Examples of Unsecured Loans in India

- Personal loan: Generally taken to cover medical emergencies, foreign trips, or large purchases.

- Instant Card Loans: You can take quick loans up to the limit of your card.

- Education Loans (occasionally): In the absence of collateral backing.

- Consumer Durable Loans: To buy electronics or appliances unsecured.

Key terms to remember:

- Credit Score: A three-digit number summarizing how responsibly you’ve repaid past credit accounts and loans.

- Debt-to-Income Ratio: The lenders verify if the remaining income is sufficient to fund another loan.

- Pre-Approval: Most unsecured loans are pre-approved on the basis of credit and/or banking relationships.

Key Differences Between Secured and Unsecured Loans

Here’s a simple comparison to give you a better idea of how these loan types compare to one another:

Feature | Secured Loan | Unsecured Loan |

Collateral Required | Yes (i.e., home, car) | No |

Interest Rate | Lower (as low as 7-9% for housing loans) | Higher (between 10% to 24% or even more) |

Loan Eligibility | Depending on asset value and borrower profile | Depending on income, credit history and credit score |

Risk to Borrower | Loss of asset in case of default | No asset is lost but the credit score is negatively affected |

Loan amount | Higher in general | Lower |

Repayment Term | Up to a maximum of 30 years for home loans | 12-60 months |

Processing Time | Lengthier, as a result of legal verification of collateral | Quicker—usually in 48 hours |

Also Read: How to Get a Personal Loan with Low Interest Rate in India (2025)

Pros and Cons of Each

Advantages of Secured Loans

- Decreased interest rates

- Increased loan sizes

- Longer repayment period

Disadvantages of Secured Loans

- Asset risk—risk of losing property or a car

- Greater processing time

- Needs to involve asset verification documents

Advantages of Unsecured Loans

- No collateral required

- Instant approval and disbursement

- Flexible usage (no limit on end-use)

Drawbacks of Unsecured Loans

- Higher interest rates

- Strict eligibility requirements

- Reduced lending limit

Which Type of Loan Best Suits You?

The choice between a secured loan and an unsecured loan is a function of your risk tolerance and financial requirements and priorities.

Here is a simple guide:

Select a secured loan if:

- You require a substantial loan amount (such as to buy a house)

- You’re agreeing to pledge an asset

- You are seeking decreased interest rates and extended EMIs

Select an unsecured loan if:

- You require instant cash

- You do not wish to mortgage your assets

- You’re positive about your credit and income history

Also, if you have a low credit score, securing an unsecured loan may be difficult, but a secured loan may still be available if you do possess an asset to pledge as collateral.

Frequently Asked Questions (FAQs)

- Do I qualify to receive a secured loan without a credit history?

Yes, as the lender depends more on the value of the collateral as compared to your credit score. - What if I fall behind on a secured loan?

The lender has a legal right to seize the pledged asset in order to recover the debt. - Which is better, a gold loan or a personal loan?

It depends—personal loans are better if you don’t wish to make a gold pledge and possess a good credit history. Gold loans are available at a relatively low interest rate. - Can I convert an unsecured loan into a secured loan?

Not typically. Some lenders do permit you to refinance your loan in exchange for pledging an asset—particularly when in financial difficulties. - Does an unsecured loan impact my credit score more?

Yes, defaults on unsecured loans do result in steeper declines in your credit score because there is no asset to fall back on. - Which loan option is simpler to obtain?

Unsecured loans are simpler and quicker to apply for when you have a good credit record. Secured loans are more time-consuming and require more paperwork.

Conclusion: The Right Move with Your Money

So, the bottom line on secured versus unsecured loans? Simply risk versus reward—yours and the lenders’. Depending on whether you need larger amounts, less interest, and a longer period of time to pay back, secured loans are probably your best option (as long as you don’t mind putting up a possession). Otherwise, if speed and flexibility are more important to you, look to unsecured loans.

Whatever option, always keep in mind your repayment ability, financial objectives, and risk tolerance. Loans can empower you if used thoughtfully. Stay tuned to MoneyPocket.in for more tips on finance, EMI calculators, and practical money tips!

One Comment